What Is a Fixed Annuity? A Guide to Guaranteed Retirement Stability in 2026

- dcjrichards

- 6 days ago

- 7 min read

What if you could stop checking the stock market every morning and finally feel like your retirement savings are anchored in calm waters? It's a heavy burden to carry the fear that a sudden market downturn might erode the principal you spent decades building. You likely believe that your hard-earned savings should be protected, not gambled. A fixed annuity serves as a protective mentor for your portfolio, converting that lingering economic uncertainty into a steady, predictable source of personal security.

This guide will clarify how a fixed annuity provides guaranteed interest rates, with 2026 market peaks reaching as high as 6.50% for specific multi-year terms. You'll learn how to secure a lifetime income stream and take advantage of the strong creditor protections available to Florida residents. We'll walk through the latest NAIC best interest standards and explain how these tools provide a safe refuge for your future. Let's explore how to replace your anxiety with the quiet confidence of a guaranteed retirement anchor.

What Is a Fixed Annuity? Your Financial Anchor in an Uncertain Market

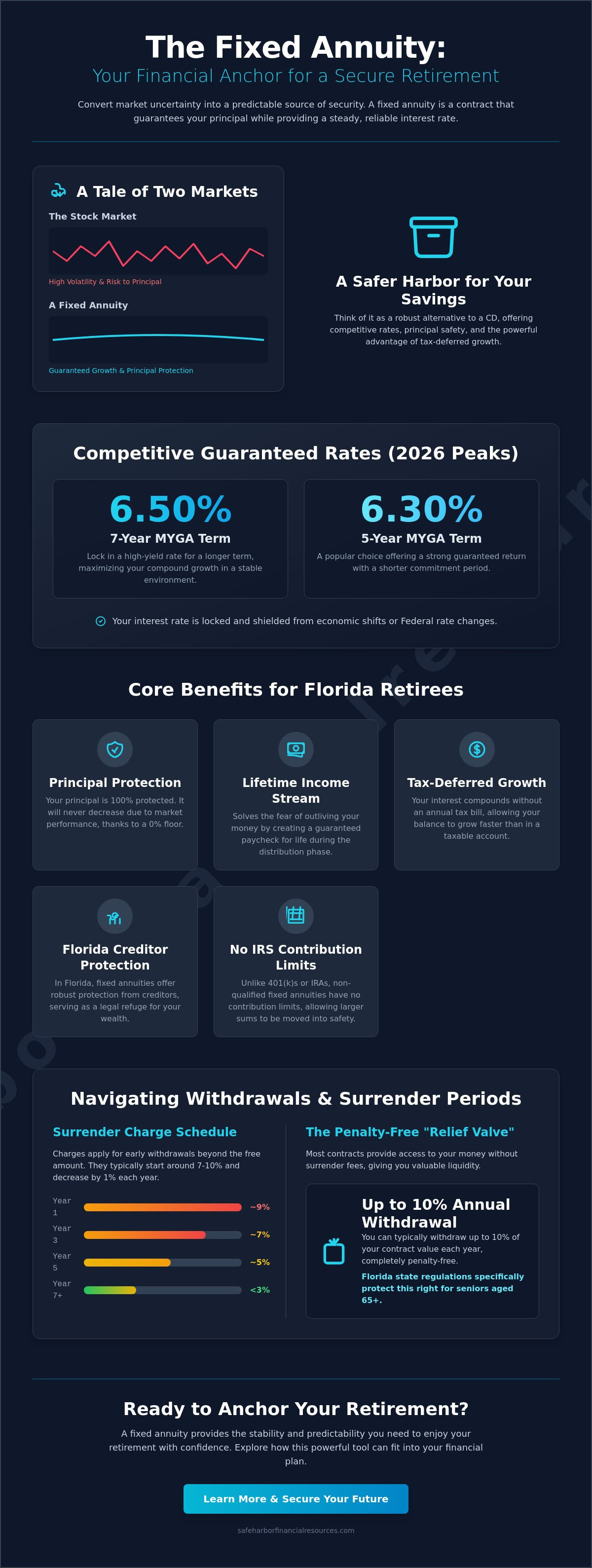

Think of a fixed annuity as a sturdy vessel anchored in a protected bay while the open ocean of the stock market tosses and turns. It's a formal agreement between you and an insurance company. You provide a lump sum or periodic payments, and in return, the insurer promises to keep your principal safe while adding a steady stream of interest. This relationship transforms your retirement planning from a source of stress into a celebration of your hard-earned milestones.

During the accumulation phase, your savings grow without the anxiety of market volatility. Many retirees view these accounts as a more robust version of a high-yield certificate of deposit (CD). They offer similar predictability but often come with more competitive rates and the benefit of tax-deferred growth. It creates a predictable environment where you can watch your wealth grow without the constant fear of a sudden market drop.

To better understand this concept, watch this helpful video:

How the Fixed Interest Rate Works

In May 2026, the landscape for fixed rates is particularly strong. For example, some 7-year multi-year guaranteed annuities (MYGAs) are offering rates as high as 6.50%, while 5-year options typically sit around 6.30%. The insurance company sets a guaranteed minimum interest rate that stays locked for your chosen term. This means you aren't at the mercy of fluctuating federal rates or economic shifts. A fixed annuity acts as a shield, ensuring your retirement principal never decreases due to market performance.

The Role of the Insurance Carrier

The stability of your retirement anchor rests on the financial strength of the carrier you choose. These companies don't gamble with your future; instead, they invest your premiums into high-quality, stable corporate and government bonds. This conservative approach allows them to fulfill their promise of safety. By choosing an insurer with high ratings, you're partnering with a guardian that has the expertise to handle complex industry landscapes while keeping your personal well-being as the top priority.

The Core Benefits: Why Florida Retirees Choose Fixed Annuities

Florida is home to some of the most beautiful retirement milestones, and for many in Palm Beach Gardens, protecting those moments requires a reliable financial anchor. A fixed annuity is often the first choice because it guarantees your principal remains untouched by market storms. While other investments might keep you awake at night, this vehicle ensures that every dollar you contribute is shielded from loss. In our state, these contracts also offer robust creditor protection, serving as a legal refuge for your hard-earned wealth.

Beyond protection, tax-deferred growth allows your interest to compound without an annual tax bill from the IRS. This is especially valuable for those in higher tax brackets, as it lets your balance grow faster than it would in a taxable account. Modern annuities also emphasize living benefits, providing security you can use during your lifetime rather than just a legacy for others. Unlike IRAs or 401(k)s, there are no IRS contribution limits on non-qualified fixed annuities, giving you the freedom to move larger sums into safety whenever you're ready.

Creating a Guaranteed Stream of Lifetime Income

The transition from saving to spending, known as the distribution phase, is where the fixed annuity truly shines. It solves the universal fear of outliving your money by providing a paycheck that never stops. You can choose a "Life Only" payout for maximum monthly income or a "Period Certain" option to ensure payments continue for a specific timeframe to your beneficiaries. This predictable income perfectly complements Social Security, providing a double layer of insulation for your lifestyle and your peace of mind.

Safety from Market Volatility

While direct stock market investing can feel like a rollercoaster, an annuity offers a level horizon. Even when the market experiences a downturn, your account maintains a 0% floor, meaning you never lose value due to index performance. For regular updates on maintaining your financial peace of mind, you can follow Safe Harbor on Facebook. If you want to see how these benefits apply to your specific situation, it's helpful to consult with a professional guide who understands the local Florida landscape.

Is a Fixed Annuity Right for Your Retirement Voyage?

Determining if a fixed annuity is the right vessel for your future depends on your personal "safe harbor" requirements. While some retirees seek the slightly higher growth potential found in fixed indexed annuities, others prefer the absolute certainty of a guaranteed interest rate. It's about matching your financial engine to the specific waters you plan to sail during your Florida retirement. Your decision should align with your total strategy, ensuring your principal is protected while your income remains predictable.

Navigating Surrender Periods and Fees

Most contracts in 2026 include a surrender charge if you withdraw more than the allowed amount early. These charges often start between 7% and 10% in the first year. They typically decrease by 1% annually over a six to ten year period. However, most plans provide a relief valve. You can usually withdraw up to 10% of your contract value annually without any penalty from the insurer. In Florida, state regulations specifically protect seniors aged 65 or older by ensuring they have access to this 10% withdrawal provision without surrender fees. It's vital to plan for your liquidity needs so your anchor doesn't become a chain. Remember that withdrawals before age 59½ may also trigger a 10% IRS penalty on taxable amounts.

The Value of a Local Palm Beach Gardens Expert

Generic online calculators can't capture the nuances of living in Palm Beach County. They don't understand the local lifestyle or the specific creditor protections available to Florida residents. A personalized assessment is far superior to a digital estimate. By working with a local professional who acts as a knowledgeable ally, you ensure your strategy is built on integrity and precision. We invite you to find your steady ground through a complimentary professional assessment. You can connect with us and stay informed by visiting Dennis Richards on Facebook to begin your journey toward a more secure and celebratory retirement.

Charting Your Course Toward a Worry-Free Retirement

You've spent decades navigating the unpredictable currents of the financial world to reach this milestone. Now, it's time to move from the stress of accumulation to the celebration of a secure lifestyle. A fixed annuity acts as your final anchor, ensuring the wealth you've built remains protected regardless of how the market behaves. By choosing a path centered on principal safety and living benefits, you're not just planning for the future; you're protecting your peace of mind today.

Every retirement voyage is unique. Your strategy should reflect the specific landscape of Palm Beach Gardens and the unique protections available in Florida. Generic advice often misses the precision required to match a plan to your actual life goals. We provide personalized, maritime-themed financial guidance that prioritizes your security above all else. Our team is ready to act as your knowledgeable ally, helping you find the steady ground you deserve.

Your retirement should be a time of refuge and joy, not a source of constant concern. Let's work together to ensure your financial harbor is as calm and reliable as it can be.

Common Questions About Retirement Stability

How does a fixed annuity differ from a fixed indexed annuity?

A standard fixed annuity provides a specific, guaranteed interest rate for a set period, while a fixed indexed annuity bases its interest on the performance of a market index. While the indexed version offers the potential for higher growth, the traditional fixed option gives you the absolute certainty of a locked-in rate. Both products protect your principal from market losses, acting as a safe harbor for your retirement savings.

Can I lose money in a fixed annuity if the stock market crashes?

You cannot lose your principal or earned interest in a fixed annuity due to a stock market crash. The insurance company assumes all the investment risk, guaranteeing that your account value will only grow or stay the same. This protection creates a reliable financial anchor, allowing you to celebrate your retirement milestones without the anxiety of watching ticker tapes or worrying about economic volatility.

What happens to my fixed annuity if I pass away before the payout phase?

If you pass away before the payout phase begins, the full value of your account is typically paid directly to your named beneficiaries. This process usually bypasses the delays and costs of probate, providing your loved ones with a swift and secure transition of assets. It ensures that your legacy remains a source of stability for your family, mirroring the protective role the annuity played during your lifetime.

Is the interest earned on a fixed annuity taxable every year?

Interest earned on a fixed annuity is not taxable every year; instead, it grows on a tax-deferred basis until you make a withdrawal. This allows your savings to compound more efficiently because you aren't losing a portion of your gains to annual taxes. When you eventually take money out, you only pay ordinary income tax on the interest portion, assuming you used after-tax dollars to fund the contract.

Comments