Medigap Plans in 2026: Navigating Your Medicare Supplement Options

- dcjrichards

- May 10

- 7 min read

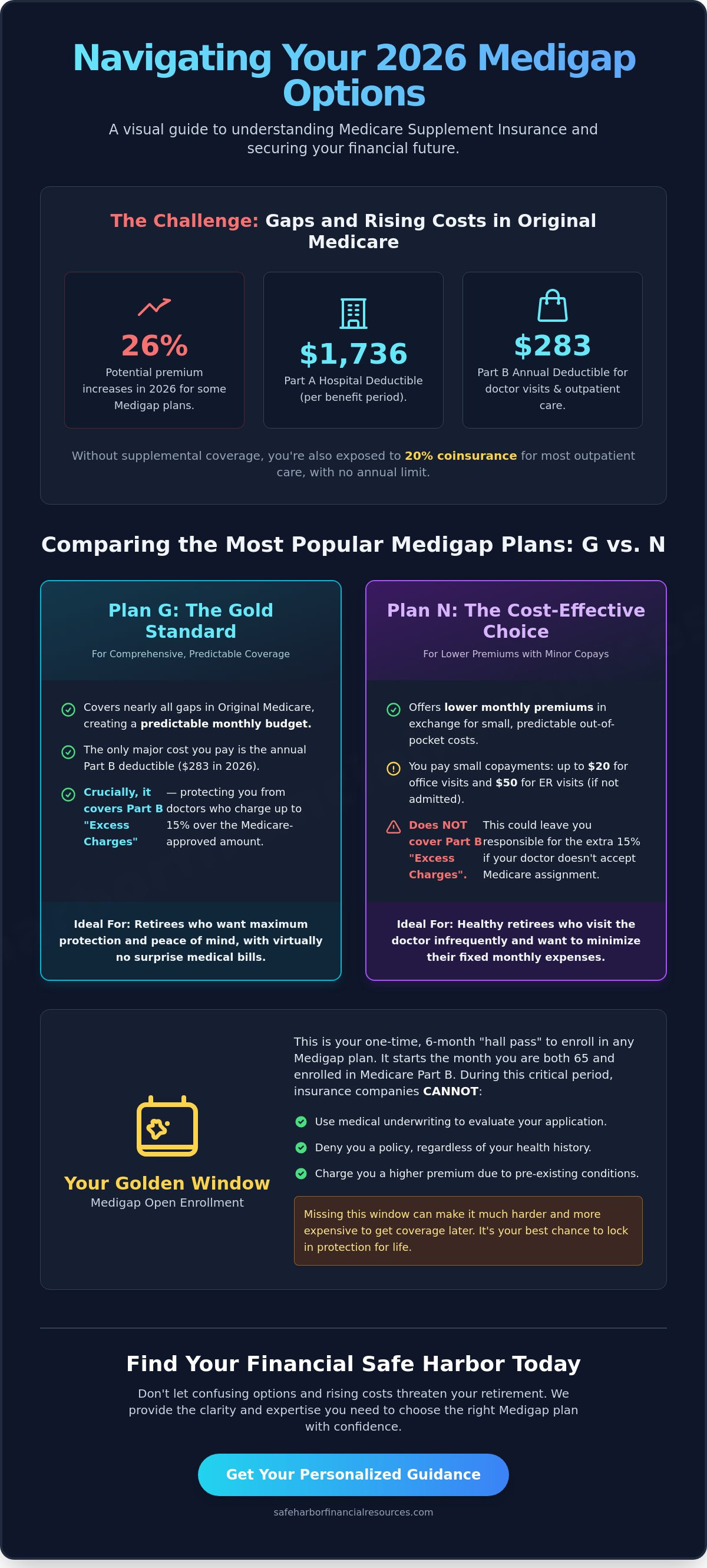

Did you know that early 2026 filings show some medigap plans are seeing premium increases as high as 26%? It's a startling figure that can quickly turn your 65th birthday celebration into a season of worry. You've worked hard for your retirement, and you deserve to feel secure rather than anxious about the $283 Part B annual deductible or the $1,736 Part A hospital deductible. It's completely normal to feel confused when comparing options like Plan G and Plan N, especially with the new restrictions on Plan N that began on April 9, 2026.

At Safe Harbor Financial Resources, we believe your healthcare should be a source of stability, not a series of tough questions. This article will show you how to eliminate unpredictable out-of-pocket costs and find a plan that lets you keep your favorite doctors. We'll explore the latest 2026 rate trends, explain why 440,000 people recently moved from Medicare Advantage back to supplemental coverage, and help you lock in a predictable monthly budget for the years ahead. It's time to find your financial safe harbor and protect your savings for good.

Navigating the Gaps: What Medigap Plans Mean for Your 2026 Medicare Coverage

Medicare Part A and Part B provide a solid foundation, but they don't cover everything. You might find yourself facing a $1,736 hospital deductible per benefit period or a $283 annual deductible for doctor visits. For many, What is Medigap? becomes the central question when planning a secure retirement. Essentially, medigap plans serve as the bridge between government coverage and total financial security.

To better understand this concept, watch this helpful video:

In 2026, medigap plans remain standardized by federal law. This means the medical benefits for a Plan G policy from one company are identical to Plan G from another. While the coverage is the same, the premiums can vary wildly. Early 2026 filings show some carriers raising rates by over 12% to 26%, making it vital to have a trusted ally who can help you find the most stable pricing. Relying on Original Medicare alone leaves you exposed to 20% coinsurance for outpatient care, which can be financially devastating without a "Safe Harbor" to protect your savings.

The Role of Supplemental Insurance in Palm Beach County

Living in Palm Beach Gardens gives you access to world-class medical facilities, but specialized care in South Florida often comes with a high price tag. One of the greatest benefits of these supplements is the freedom they provide. You aren't restricted by the narrow networks often found in Advantage plans. You can visit any doctor or specialist in Palm Beach County who accepts Medicare. When you move from an employer plan to retirement, you need accurate answers to avoid penalties or coverage gaps. We focus on providing that clarity so your 65th birthday is a milestone to celebrate, not a source of stress.

Comparing Your Options: Plan G, Plan N, and Florida Standardization

Choosing between medigap plans doesn't have to be a source of anxiety. In 2026, Plan G remains the gold standard for new enrollees because it covers every single gap in Original Medicare except for the $283 Part B annual deductible. It's the preferred choice for those who want a predictable monthly healthcare budget without any surprises at the doctor's office. Plan N serves as a cost-effective alternative for retirees who are comfortable paying small copayments, such as $20 for some office visits or $50 for emergency room visits that don't result in an admission. The choice between these two options typically comes down to whether you prefer a higher, predictable monthly premium with Plan G or the lower monthly costs and variable copays of Plan N.

Florida’s unique market adds another layer of security for you. Because medigap plans in Florida are standardized, you can be certain that Plan G benefits are identical whether you buy from a small local carrier or a market leader. However, premium stability is where the "tough questions" come in. With the top ten companies holding 69% of the market as of late 2024, it's vital to look at a carrier's history of rate increases rather than just the initial price. If you want to dive deeper into the rules, the official Medicare website provides a full breakdown of these enrollment regulations.

Plan G vs. Plan N: Balancing Premium Costs and Protection

One critical difference involves Part B excess charges. In Florida, if a provider doesn't accept "assignment," they can charge up to 15% more than the Medicare-approved amount. Plan G protects you from these extra costs, while Plan N does not. This makes Plan G a safer harbor for those who see many specialists. Healthy retirees who want to keep their fixed costs low often find Plan N to be a perfect fit, though it's important to remember that as of April 9, 2026, Plan N is no longer available in many Guaranteed Issue situations in most states. If you missed the window for Plan F, which was phased out for new enrollees on January 1, 2020, these two options are your primary paths to security. If you feel stuck between these choices, you can connect with us for personalized guidance to find your best fit.

Finding Your Safe Harbor: When and How to Enroll in Medigap

The Medigap Open Enrollment Period acts as your one-time "hall pass" to secure long-term health security. For six months, starting the day you're both 65 and enrolled in Part B, insurance companies are prohibited from using medical underwriting to deny you a policy. They can't charge you more for pre-existing conditions or past health history. This window is your best chance to find a permanent financial safe harbor. While many people approach this milestone with anxiety, we believe your 65th birthday should be a great celebration. It's a reward for years of hard work, not a reason for confusion and concern.

Starting early is the key to a smooth transition. You can review the official Medicare guide to Medigap for the basic federal rules, but local expertise helps you narrow down the best choices in Palm Beach Gardens. If you're moving from an employer-sponsored plan, you need a clear strategy to avoid coverage gaps. We help you ask the tough questions about carrier stability and network access so you can enjoy your retirement with total peace of mind. Our goal is to provide the accurate answers you need to choose between medigap plans with confidence.

The 65th Birthday Milestone: A Supportive Timeline

A simple timeline can replace stress with stability. We suggest a three-month lead time to ensure everything is in place for your Medicare effective date. This proactive approach helps you avoid late enrollment penalties, which can permanently increase your monthly costs. Follow these steps to stay on track:

3 Months Before: Apply for Medicare Part A and B through Social Security to ensure your enrollment is processed in time.

2 Months Before: Compare the standardized medigap plans available in Florida and check for the most stable rate histories.

1 Month Before: Submit your application so your new ID cards arrive before your birthday month begins.

Following this schedule ensures your coverage is active the moment you need it. We are here to act as your trusted ally throughout this entire process, making sure no detail is overlooked. If you're ready to secure your future and protect your savings, reach out to us for a FREE consultation on your Medicare options.

Secure Your Financial Future with Confidence

Your retirement should be a time of peace and predictability, not a period of financial anxiety. We've explored how medigap plans bridge the gap between Original Medicare and total security, especially as we face the 2026 rate shifts and plan restrictions. Whether you choose the comprehensive protection of Plan G or the cost-effective structure of Plan N, the goal is to find a stable solution that fits your lifestyle. Your six-month Open Enrollment window remains the most powerful tool you have to secure coverage regardless of your health status.

Navigating these choices alone can feel like a chore, but you have a trusted ally nearby. With our local Palm Beach Gardens expertise and a customer-comes-first philosophy, we provide the accurate answers you need for every 2026 Medicare change. We invite you to Ask us the tough questions during a FREE Medigap consultation. Let us help you turn your 65th birthday into the great celebration it deserves to be. You've earned this long-term security, and we're here to ensure you find your safe harbor.

Frequently Asked Questions

Is Plan G the best Medigap plan for Florida residents in 2026?

Plan G is widely considered the gold standard for Florida residents in 2026 because it offers the most comprehensive protection available to new enrollees. It covers all medical gaps except for the $283 Part B annual deductible. This makes it a perfect fit for those who want a predictable budget without worrying about 20% coinsurance or Part B excess charges. While Plan N is a cost-effective alternative, Plan G remains the top choice for total peace of mind.

Can I change my Medigap plan later if my health needs change?

You can apply to change your medigap plans at any time, but you'll likely have to answer health questions and pass medical underwriting. Unlike some other states, Florida does not have a "birthday rule" that allows for automatic annual switches. This is why your initial six-month Open Enrollment Period is so critical. Choosing the right plan from the start ensures you have a permanent safe harbor even if your health needs change down the road.

Do Medigap plans include prescription drug coverage (Part D)?

Medigap policies don't include prescription drug coverage, so you'll need to enroll in a separate Medicare Part D plan. For 2026, the maximum annual deductible for Part D plans is $615. We help our neighbors in Palm Beach Gardens coordinate these two separate pieces of the puzzle to ensure there are no gaps in their protection. Having both a supplement and a drug plan provides a complete shield against high healthcare costs.

What happens to my Medigap coverage if I move out of Palm Beach County?

Your coverage is fully portable and will follow you anywhere in the United States. Unlike Medicare Advantage plans that rely on local provider networks, these supplements allow you to see any doctor who accepts Medicare. If you move away from Palm Beach County, you don't need to worry about losing your benefits or finding a new policy. This flexibility is one of the primary reasons retirees value medigap plans for long-term security.

Comments