Immediate Annuity Guide for Palm Beach Gardens Retirees (2026)

- dcjrichards

- May 2

- 13 min read

What if your retirement wasn't a gamble on the S&P 500, but a guaranteed monthly deposit as reliable as the Florida sunrise? For many retirees in Palm Beach Gardens, the dream of relaxing sunset years feels clouded by market volatility and the looming shadow of RMD requirements. You've worked hard to build your nest egg, and it's frustrating to feel like you're constantly defending it against economic storms rather than enjoying the life you've earned.

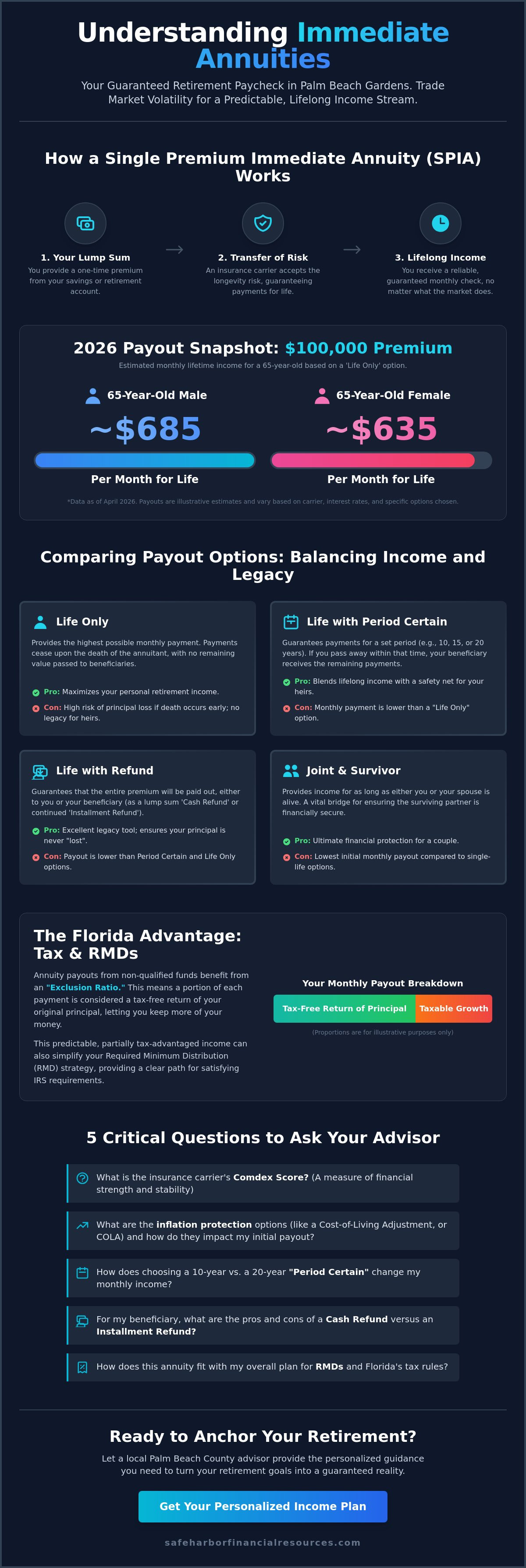

We believe your 60s and 70s should be a time for celebration, not concern. By choosing an immediate annuity, you can secure a predictable paycheck that lasts as long as you do. As of April 2026, a $100,000 premium could provide a 65-year-old male with roughly $685 per month for life, while a female of the same age could see about $635. This guide will show you how to anchor your financial plan against uncertainty. We'll break down the latest 2026 payout trends, explain how the new NAIC Valuation Manual affects your options, and show you how Florida's strict best interest standards ensure your protection remains the top priority.

Key Takeaways

Discover how to trade the stress of market volatility for a "Safe Harbor" by securing a predictable income stream that never runs dry.

Compare different payout structures to see if an immediate annuity with "period certain" features or joint survivor benefits best fits your family’s legacy goals.

Learn how Florida’s specific tax rules and the "exclusion ratio" can help you keep more of your money while simplifying your annual RMD requirements.

Get a checklist of the five essential questions to ask about carrier Comdex scores and inflation protection to ensure your security lasts for decades.

Understand why a local Palm Beach County advisor offers the personalized guidance you need to turn a 65th birthday into a true celebration of financial freedom.

Table of Contents What is an Immediate Annuity? Your Palm Beach Paycheck Explained Comparing Immediate Annuity Payout Options: Which is Right for You? The Florida Advantage: Tax Treatment and RMD Planning Buying Guide: 5 Critical Questions to Ask Before You Commit The Safe Harbor Approach: Local Expertise in Palm Beach Gardens

What is an Immediate Annuity? Your Palm Beach Paycheck Explained

Living in Palm Beach Gardens is a privilege, but it's one that requires a steady hand on the tiller. Many of our neighbors spend decades building a nest egg, only to find that the transition into retirement brings a new kind of anxiety. This is where the concept of a "Safe Harbor" becomes more than just a name; it’s a strategy for peace of mind. An immediate annuity acts as a strategic anchor, allowing you to trade a portion of your savings for a guaranteed, lifelong income harbor that market storms cannot touch.

So, What is an Immediate Annuity? At its core, a Single Premium Immediate Annuity (SPIA) is a contract with a highly rated insurance company. You provide a lump sum upfront, and in return, the insurer commits to sending you a check every single month for the rest of your life. In the current 2026 economic environment, where interest rates have stabilized and product transparency has increased due to recent NAIC valuation updates, many local retirees find this an ideal time to lock in a payout that supports their unique lifestyle.

The SPIA Mechanism: How Your Lump Sum Becomes Income

When you enter into an annuitization agreement, you're not just opening another savings account. You're creating a private pension. The insurance carrier uses its financial strength, often backed by strong Standard & Poor’s ratings, to guarantee these payments regardless of what happens on Wall Street. An immediate annuity represents a transfer of longevity risk from the individual to the insurance company. This mechanism ensures that even if you live to be 105, the checks will continue to arrive on the first of the month just like clockwork.

Why Palm Beach Gardens Retirees Choose Immediate Income

Life in Palm Beach County comes with specific financial demands. Between rising HOA fees in gated communities, Florida property taxes, and the cost of premium Medicare supplements, fixed expenses can be high. Relying solely on a volatile brokerage account to cover these non-negotiables often leads to unnecessary stress. By supplementing Social Security with a guaranteed annuity payout, you create a "Sleep Well at Night" (SWAN) factor. It marks a profound psychological shift. You move from the defensive posture of accumulating wealth to the joyful freedom of spending it. This allows you to enjoy our local golf courses and dining with total confidence, knowing your foundational costs are already covered by a secure, local financial plan.

Comparing Immediate Annuity Payout Options: Which is Right for You?

Choosing the right payout structure for your immediate annuity is a deeply personal decision that balances your need for maximum income with your desire to protect your loved ones. While the "Life Only" option provides the largest monthly check, it comes with a significant trade-off: payments cease the moment you pass away. For many retirees in Palm Beach Gardens, this feels like a risk that doesn't align with their protective instincts. To help clarify these choices, the Insurance Information Institute explains immediate annuities can be customized with "Period Certain" or refund features. These additions ensure that if you pass away before a set timeframe, such as 15 or 20 years, your beneficiaries continue to receive the remaining value. It's about creating a safety net that fits your specific family history and health status.

Cash Refund and Installment Refund options are also excellent tools for those worried about "losing" their principal to the insurance company. A Cash Refund pays your beneficiary the difference between your initial premium and the total payments you received in one lump sum. An Installment Refund provides the same protection but continues the monthly checks until the principal is fully returned. These features transform your contract into a legacy tool, ensuring your hard-earned savings stay within your family regardless of how long you live.

Single Life vs. Joint Life: A Strategic Framework

Consider a couple living in a community like Frenchman's Creek. If one spouse has a robust pension but the other doesn't, a Joint and Survivor immediate annuity acts as a vital bridge. This option ensures that even after the first spouse passes, the survivor continues to receive a check for the rest of their life. While the monthly amount is slightly lower than a single life policy, the security it provides for a surviving spouse is often the most important factor in a long-term plan. If you're weighing these trade-offs, you can ask us the tough questions about which survivor percentage makes the most sense for your household.

Addressing the Inflation Objection: COLA and Riders

In 2026, protecting your purchasing power against rising costs is a top priority. You can add a Cost of Living Adjustment (COLA) rider to your contract, which increases your payout by a set percentage each year. However, keep in mind this usually reduces your starting income. An alternative strategy gaining traction this year is laddering. Instead of committing all your funds to one contract today, you purchase smaller annuities over several years. This approach allows you to capture potentially higher rates in the future and step up your income as your Palm Beach County expenses grow.

The Florida Advantage: Tax Treatment and RMD Planning

Florida is widely known as a retirement paradise, but the benefits go far beyond our beautiful beaches and world-class golf courses. For retirees in Palm Beach Gardens, the state's tax structure provides a significant boost to the efficiency of an immediate annuity. Because Florida has no state income tax, every dollar of your annuity payout stays in your pocket rather than being diverted to Tallahassee. This lack of a "state haircut" means your net retirement paycheck is often 5% to 10% higher than it would be for a retiree living in a high-tax state like New York or Illinois.

The tax efficiency of these contracts also depends on the source of your funds. If you use "non-qualified" money, such as savings from a brokerage account, you benefit from the Exclusion Ratio. This rule acknowledges that a portion of each check is simply a return of your original, already-taxed principal. Only the earnings portion is subject to federal income tax. This creates a predictable, tax-favored income stream that helps you maintain your lifestyle without the constant worry of shifting tax brackets.

Solving the RMD Headache for Palm Beach County Seniors

As you reach the age for Required Minimum Distributions (RMDs), managing multiple retirement accounts can lead to unnecessary confusion and concern. If you purchase an immediate annuity using "qualified" funds from a Traditional IRA or 401(k), the process becomes much simpler. The IRS considers the scheduled payments from an annuitized qualified account to satisfy the Required Minimum Distribution for that specific contract automatically. This automation removes the risk of forgetting a distribution and facing the steep 25% penalty that applies in 2026. It also helps prevent the "tax torpedo" effect, where large, lumpy RMD withdrawals can unexpectedly push your Social Security benefits into a higher taxable tier.

Asset Protection Benefits in Florida

We often speak about finding a "Safe Harbor" for your finances, and in Florida, this metaphor is backed by law. Florida Statute 222.14 provides some of the strongest asset protection in the country for annuity owners. In most cases, the cash value and the income stream from an annuity are protected from the claims of creditors. For high-net-worth residents in Palm Beach Gardens, this adds a vital layer of security to their estate plan. It ensures that your foundational income remains a protected sanctuary, allowing you to focus on celebration and family rather than legal or financial vulnerability. Integrating these protections into your broader plan provides the calm and stability you deserve during your 65th birthday milestones and beyond.

Buying Guide: 5 Critical Questions to Ask Before You Commit

Deciding to secure an immediate annuity is a significant step toward a stable retirement, but not every contract is built the same. In the busy Palm Beach Gardens financial market, you'll find a wide range of offers that look similar on the surface but carry very different long-term implications. Before you sign any paperwork, you need to ask the tough questions to ensure your "Safe Harbor" is actually built on solid ground. Don't settle for the first quote you see. Data from April 2026 shows that the difference between the best and worst immediate annuity quotes can result in a gap of hundreds of dollars per month for the rest of your life. To help you navigate this, we've identified five essential questions you must ask your broker.

What is the carrier’s Comdex score and Standard & Poor’s rating? You're trusting this company to pay you for decades. Their financial backbone matters.

Is this a fixed amount or does it include an inflation hedge? A payout that feels generous today might not cover your HOA fees or healthcare costs in ten years.

What happens to the remaining balance if I pass away tomorrow? Ensure you understand whether your heirs are protected or if the insurer keeps the principal.

How does this specific payout compare to the current 2026 market average? With new NAIC valuation rules in effect as of January 1, 2026, pricing has shifted across the industry.

Am I using the right "bucket" of money? Choosing between Qualified (IRA) and Non-Qualified (brokerage) funds changes your tax liability and RMD automation.

Evaluating Carrier Strength and Reliability

In our office, we believe protection comes first. We generally advise against any carrier rated below an "A" by major agencies. While the Florida Life & Health Insurance Guaranty Association provides a safety net for residents, your first line of defense should always be the carrier's own balance sheet. We vet every company using the Comdex score, which averages ratings from all major agencies into one easy-to-understand number. This ensures our local clients are anchored with only the most stable institutions in the country.

Avoiding the 'Principal Loss' Trap

One of the biggest sources of confusion and concern for retirees is the fear that their money will vanish if they die early. While a "Life Only" immediate annuity offers the highest possible monthly check, it's often a mistake for those who want to leave a legacy for their children or spouse. Adding a "Refund" feature ensures that any unused portion of your premium is returned to your beneficiaries. It's a small trade-off in monthly income for a massive gain in peace of mind. If you want to see how these different riders impact your specific numbers, you can schedule your free consultation with our local team today.

The Safe Harbor Approach: Local Expertise in Palm Beach Gardens

Digital algorithms are useful for a quick glance, but they lack the empathy required to build a true lifetime security plan. While many national websites promise a "no agent" experience, we believe that your retirement deserves a human touch. Your 65th birthday is a milestone that should be celebrated with confidence, not clouded by the confusion of a cold, automated quote engine. In Palm Beach Gardens, we don't just provide a contract; we offer a relationship built on integrity and professional competence. We're your neighbors, and we understand that your goals are about more than just numbers on a screen.

Our philosophy is simple. We want you to ask us the tough questions about your financial future. Whether you're worried about the 2026 changes to the NAIC Valuation Manual or you're unsure how an immediate annuity fits with your current estate plan, we provide the accurate answers you need to feel secure. By taking a protective stance, we ensure that every decision you make serves as a steady hand in an often complex world. We're personally invested in your happiness and long term stability.

Personalized Retirement Strategies vs. Digital Algorithms

A face to face consultation in our Palm Beach Gardens office allows us to see the full picture of your life. We don't look at your income in a vacuum. Instead, we integrate your immediate annuity strategy with your existing Medicare Supplement plans and life insurance coverage. This holistic approach ensures that your monthly "paycheck" isn't just a fixed sum, but a strategic anchor that protects your entire lifestyle from market storms. We help you move from a state of uncertainty to a state of complete understanding, replacing anxiety with the calm of a safe harbor.

Your Next Steps: Securing Your Lifetime Income

Preparing for your future shouldn't be a source of stress. When you come in for a visit, we make the process unhurried and logical. To get the most out of our time together, we recommend gathering a few key documents that will help us tailor a plan specifically for you. These include:

Current Traditional or Roth IRA statements.

Estimates from any employer-sponsored pensions.

Your most recent Social Security benefit statement.

Details of your current healthcare and Medicare coverage.

Having these items ready allows us to provide a high level of professional authority while maintaining that warm, neighborly touch you expect from a local expert. It’s time to stop wondering if your savings will last and start enjoying the retirement you’ve worked so hard to build. Schedule your free retirement income review in Palm Beach Gardens today and let us help you turn your hard earned savings into a guaranteed lifetime paycheck.

Chart Your Course to a Worry Free Retirement

Retirement shouldn't be a time for confusion and concern. It's a major life milestone that deserves a great celebration. Throughout this guide, we've explored how an immediate annuity can transform your hard earned savings into a predictable monthly paycheck tailored specifically for your life in Palm Beach Gardens. From the 2026 tax efficiencies unique to Florida to the seamless automation of your RMD requirements, these strategies provide the calm and stability you've worked decades to achieve.

As your protective guide, we specialize in retiree security and offer expert guidance on every detail of your income plan. We provide direct access to top rated Florida insurance carriers and help you vet every option with professional authority and a warm, neighborly touch. It is time to replace market anxiety with the peace of mind that comes from a steady hand and a clear plan. We invite you to ask us the tough questions and get the accurate answers you deserve.

Secure your guaranteed retirement paycheck, Get a free consultation at Safe Harbor Financial Resources

We look forward to sitting down with you and helping you find your financial safe harbor. Your future is bright, and we're here to ensure it stays that way for years to come.

Frequently Asked Questions

What is the difference between a fixed annuity and an immediate annuity?

An immediate annuity begins paying you a guaranteed income almost instantly, whereas a standard fixed annuity often refers to a deferred product used to grow your savings over time. While both offer a fixed rate of return, the immediate version is designed for those who need a reliable paycheck right now. As of April 2026, fixed rates for a 10-year term have reached 7.65%, making it a compelling time to consider which structure fits your current retirement phase.

Can I change my mind and get my money back after buying an immediate annuity?

You generally have a "free look" period of 21 days in Florida to cancel your contract for a full refund, but after that, an immediate annuity is typically irrevocable. This permanent commitment is exactly why the insurance company can guarantee a payout that lasts for the rest of your life. It's a strategic trade-off where you exchange liquidity for the ultimate security of an income stream you simply can't outlive.

How much does an immediate annuity cost in Palm Beach Gardens?

There is no set "price" for an annuity; instead, the cost is the premium amount you choose to deposit to generate your desired monthly income. Most top-rated carriers require a minimum investment of $10,000 to $25,000 to get started. Many local retirees fund these contracts using a portion of their 401(k) or proceeds from a home sale to ensure their foundational Florida living expenses are covered forever.

Is the income from an immediate annuity taxable in Florida?

Florida does not have a state income tax, so your annuity payments are completely free from state-level taxation. At the federal level, your tax liability depends on the "exclusion ratio," which treats a portion of each check as a non-taxable return of your original principal. This local tax advantage helps you keep more of your money for golf, dining, and family celebrations in Palm Beach County.

What happens to my immediate annuity if the insurance company goes bankrupt?

Your investment is protected by the Florida Life & Health Insurance Guaranty Association, which provides a safety net if a licensed carrier fails. As of 2026, this association generally covers up to $300,000 in annuity benefits for Florida residents. We prioritize your protection by only recommending carriers with high Comdex scores and strong ratings from Standard & Poor's, ensuring your "Safe Harbor" is built on a solid foundation.

How does an immediate annuity affect my Social Security taxes?

Annuity income counts toward your "provisional income," which the IRS uses to determine if your Social Security benefits are taxable. If your total income exceeds $32,000 for couples or $25,000 for individuals in 2026, up to 85% of your Social Security may become subject to federal tax. We help you look at the big picture to ensure your guaranteed income doesn't create an unexpected tax surprise.

Can I use an immediate annuity to satisfy my RMD requirements?

Yes, purchasing an immediate annuity with qualified IRA funds satisfies your Required Minimum Distribution for that specific account automatically. The IRS views these scheduled payments as meeting the distribution rules, which removes the stress of calculating annual withdrawals. This is a favorite strategy for our clients who want to simplify their finances and avoid the steep 25% penalty for missed RMDs.

What is the best age to buy an immediate annuity for maximum payout?

Payout rates increase as you get older because the insurance company bases the check amount on your life expectancy. Many retirees find that ages 70 to 75 represent a "sweet spot" for maximizing their monthly income through mortality credits. However, the best age is truly whenever you decide that peace of mind and a predictable paycheck are more important than watching the daily ups and downs of the stock market.

Comments